The Startup Equity: VC Mechanics, SAFE Notes, Cap Tables & Indian Tax Traps

Most software engineers negotiate their salary. Very few negotiate their equity — because they don't understand what it actually means. They see "0.50% equity" and either dismiss it as lottery-ticket noise or treat it as a guaranteed windfall. Both reactions are wrong, and both are expensive.

This guide is a complete technical reference for software engineers evaluating startup offers — particularly those working remotely for US-backed companies. It covers how VC funds actually work, the precise mechanics of SAFE notes and cap tables, the equity traps that silently destroy engineer payouts, and — critically for Indian engineers — the tax compliance framework that can result in criminal prosecution if ignored.

Read it once for foundational understanding. Use each module as a reference during active offer evaluation.

Table of Contents

- The Venture Capital Engine & Startup Lifecycle

- SAFE Notes & Convertible Instruments

- SaaS Metrics, Valuations & Cap Table Mechanics

- Equity Vehicles, Vesting & Option Mechanics

- Indian Tax Compliance for Remote Equity Holders

- Real-World Case Studies

- 10 Equity Traps That Destroy Engineer Payouts

- Evaluating Your Offer: A Framework

- The Negotiation Playbook

- Pre-Signing Due Diligence Checklist

MODULE 1: THE VENTURE CAPITAL ENGINE & STARTUP LIFECYCLE

To negotiate effectively, you must understand the financial incentives of the people across the table — the founders, and the VCs who fund them.

How Venture Capital Funds Work

A VC firm is not just a pool of rich people's money. It is a rigidly structured financial vehicle with a specific lifecycle, fee structure, and return mandate.

The Fund Economics:

- Management Fee (2% annually): On a $100M fund, the GPs charge $2M/year regardless of performance to cover salaries and operations. Over 10 years, this is $20M of the fund consumed before a single return.

- Carried Interest (20% of profits): After returning the original $100M to LPs, the GPs keep 20 cents of every dollar of profit. On a fund that returns $500M (a 5x return), the GPs earn $80M in carry.

- The Hurdle Rate: Many funds have an 8% annual preferred return threshold — LPs get 8% annually before the GP takes any carry.

The Power Law (Why Startups Must Scale or Die)

This is the most important concept for understanding why startups behave the way they do, why founders push so hard, and why they value shipping velocity so intensely.

In a seed portfolio of 20 companies:

| Category | # of Companies | Outcome | Return to Fund |

|---|---|---|---|

| Dead | 10 | Product fails, shuts down | $0 |

| Zombie / Walking Dead | 5 | Survives but never grows, acquired for parts | 0.5x capital back |

| Moderate Exits | 3 | Acquired for $20M-$50M | 2x-3x capital back |

| Strong Exit | 1 | Acquired for $150M-$300M | 5x-10x capital back |

| Unicorn / Fund Returner | 1 | IPO or acquired for $1B+ | 50x-100x capital back |

The Implication: The Power Law means VCs are not investing to get moderate outcomes. They need that one company to return the entire fund. This drives them to push every portfolio company toward hyper-growth, even at the cost of stability and employee wellbeing.

Engineer's Leverage: Because the startup is under constant VC pressure to ship features and grow, they desperately need senior builders who operate autonomously. If you can ship production-quality code without needing hand-holding, you are solving their most critical operational bottleneck — and your negotiating position reflects that.

The Startup Funding Lifecycle (End-to-End)

Pre-Seed Seed Series A Series B Series C+ Exit

($100k-$1M) ($1M-$5M) ($5M-$15M) ($20M-$60M) ($60M-$200M+) (IPO or M&A)

| | | | | |

2-4 people 5-15 people 15-50 people 50-150 people 150-500+ Thousands

| | | | | |

Idea/MVP PMF Search Scale PMF Hyper-growth Dominance Liquidity

| | | | | |

$2M-6M Val $6M-20M Val $20M-80M Val $100M-500M Val $500M-B+ Cash!The Sweet Spot for Equity: Seed and Post-Seed startups ($2M-$5M raised, 5-15 people, $8M-$20M valuation). These companies need senior builders immediately and have significant equity available in the ESOP pool. The risk is higher, but so is the upside.

MODULE 2: SAFE NOTES & CONVERTIBLE INSTRUMENTS

Early-stage startups almost never issue stock directly during their seed raise. The legal cost and complexity of a "priced round" (officially setting a valuation and issuing shares immediately) is $30k-$80k in legal fees alone. Instead, they use SAFE Notes — simple, fast, and cheap.

What is a SAFE Note?

Created by Y Combinator in 2013, a SAFE (Simple Agreement for Future Equity) is a legal contract where an investor gives cash to a startup today in exchange for the right to receive equity in the future — specifically, when the startup raises its first priced round (usually Series A).

Key Properties:

- Not Debt: No interest rate, no maturity date. Unlike a convertible note, the startup cannot be forced to repay a SAFE.

- Not Equity (Yet): No shares are actually issued. The investor holds a right to future shares.

- Converts Automatically: When a priced round occurs, SAFEs automatically convert into preferred stock shares.

The Two Economic Levers of a SAFE

1. Valuation Cap (The "Cap")

The maximum valuation at which the SAFE converts into equity. It rewards early risk-takers.

Example:

- Investor A puts $500,000 into a SAFE with a $8M valuation cap.

- 18 months later, the company raises a Series A at a $20M valuation.

- Investor A's $500k converts as if the company is worth $8M (not $20M).

- At $20M, $500k would buy 2.5% of the company.

- At the $8M cap, $500k buys 6.25% of the company — 2.5x more equity for taking early risk.

2. Discount Rate (The "Discount")

A guaranteed percentage reduction on the future priced round share price. Standard is 15%-20%.

Example:

- Series A share price (Preferred): $1.00 per share

- SAFE holder's effective price at 20% discount: $0.80 per share

- The SAFE investor gets 25% more shares than new Series A investors for the same dollar amount.

Cap vs. Discount — Which Applies? Upon conversion, the SAFE automatically uses whichever mechanism gives the investor more shares — usually the cap, if it's significantly below the priced round valuation.

Pre-Money vs. Post-Money SAFEs (Critical Distinction)

YC overhauled the SAFE format in 2018, switching from Pre-Money to Post-Money SAFEs. Almost all YC companies now use post-money SAFEs.

Pre-Money SAFE (Old Format): The investor's ownership is calculated relative to the company's valuation before the round's cash lands. This was problematic — as the company added more SAFEs, early investors unknowingly diluted each other, making ownership tracking a mess.

Post-Money SAFE (New Format — What You'll Encounter): The investor's ownership is locked and calculated after the SAFE money is added.

Formula:

Investor Ownership % = SAFE Investment Amount / Post-Money Valuation CapExample: A startup raises $2.5M total across multiple SAFEs against a $12.5M post-money cap:

- Collective seed investor ownership: $2.5M / $12.5M = 20.0%

- Founders + employees know they are giving up exactly 20% — no ambiguity.

Convertible Notes (The Older Cousin)

Before SAFEs, startups used Convertible Notes — actual debt instruments with:

- An interest rate (typically 5%-8% annually)

- A maturity date (typically 18-24 months)

- A valuation cap and/or discount (same mechanics as SAFE)

Why Convertible Notes are Riskier for Startups: If the startup doesn't raise a priced round before the maturity date, the noteholders can legally demand repayment of the principal plus interest — potentially bankrupting an otherwise healthy startup.

Why You'll Still See Them: Some angels and micro-VCs prefer convertible notes because of the interest accrual. If a startup offers you a role and mentions they raised on convertible notes with a looming maturity date, this is a yellow flag — the founders may be under pressure to raise or repay.

MODULE 3: SAAS METRICS, VALUATIONS & CAP TABLE MECHANICS

Core SaaS Financial Metrics

These are the numbers VCs track obsessively. Understanding them lets you evaluate whether a startup is healthy before you join.

| Metric | What It Measures | Healthy Benchmark | Red Flag |

|---|---|---|---|

| ARR | Annual Recurring Revenue (MRR × 12) | Growing 2x-3x YoY at seed | Flat or declining |

| MRR | Monthly Recurring Revenue | Predictable, growing | Lumpy / project-based |

| Net Revenue Retention (NRR) | % of revenue retained from existing customers including upsells, minus churn | 110%+ (excellent), 100%+ (good) | Below 80% (customers leaving) |

| Gross Margin | Revenue minus Cost of Goods Sold / Revenue | 70%-85% for SaaS | Below 50% |

| CAC | Cost to acquire one new paying customer | Varies by market | CAC payback > 18 months is bad |

| LTV:CAC Ratio | Lifetime customer value vs. acquisition cost | 3:1 or higher | Below 2:1 |

| Net Burn | Gross Burn minus monthly revenue | Declining over time | Increasing despite growing revenue |

| Runway | Months of cash remaining (Cash / Net Burn) | 18-24 months post-raise | Under 9 months with no term sheet |

| Churn Rate | % of paying customers canceling per month | Under 2% monthly | Over 5% monthly |

Startup Valuation Math

Startups are valued on Revenue Multiples, not profits (since most are burning cash intentionally).

Company Valuation = ARR × Revenue Multiple| Company Type | Revenue Multiple | Rationale |

|---|---|---|

| Standard B2B SaaS | 8x-12x ARR | Predictable, moderate growth |

| High-Growth SaaS (2x+ YoY) | 15x-25x ARR | Hyper-growth premium |

| AI-Native SaaS (GenAI, LLM tooling) | 30x-80x ARR | Market excitement + massive TAM |

| Infrastructure / Developer Tools | 20x-40x ARR | High stickiness, network effects |

| Consumer SaaS | 5x-8x ARR | Higher churn risk |

Real Example — Supabase (2022 Series B):

- Estimated ARR at Series B: ~$5M-$8M

- Series B raise: $80M at an estimated $500M valuation

- Implied multiple: ~65x-100x ARR

- Why? Developer tooling with massive open-source adoption = near-infinite TAM, extremely sticky, strong network effects.

The Cap Table — Full Lifecycle

The cap table is the single most important document at a startup. It determines who gets paid what during an exit.

Phase 1: Founding (Day 0)

| Stakeholder | Shares | Ownership % |

|---|---|---|

| Founder A (CEO) | 5,000,000 | 50.0% |

| Founder B (CTO) | 5,000,000 | 50.0% |

| Total | 10,000,000 | 100.0% |

Phase 2: YC Batch + Seed SAFE ($3M on $12M Post-Money Cap)

YC invests $500k at a $5M post-money cap. Additional angels add $2.5M on a $12M post-money cap.

| Stakeholder | Ownership % |

|---|---|

| Founder A (CEO) | ~37.5% |

| Founder B (CTO) | ~37.5% |

| YC (SAFE, $5M cap) | ~10.0% |

| Angel Investors (SAFE, $12M cap) | ~blended 15.0% |

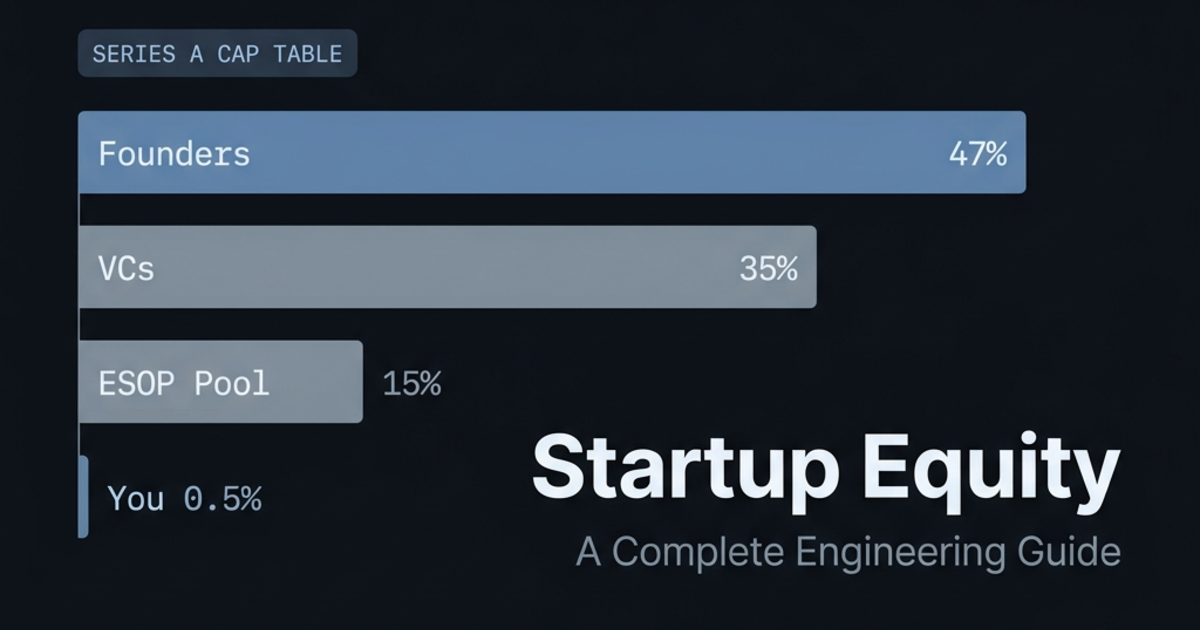

Phase 3: Series A ($6M raised at $30M pre-money, $36M post-money)

All SAFEs convert. A 15% ESOP pool is carved out before the round — diluting founders and existing holders, not new investors.

| Stakeholder | Shares | Ownership % |

|---|---|---|

| Founder A | 5,000,000 | 23.1% |

| Founder B | 5,000,000 | 23.1% |

| YC (Converted) | 1,300,000 | 6.0% |

| Angels (Converted) | 2,200,000 | 10.2% |

| ESOP Pool (Employees) | 3,250,000 | 15.0% |

| Series A Investors | 4,900,000 | 22.6% |

| Total | 21,650,000 | 100% |

An engineer joining here might receive 0.50% = 108,250 options.

- Paper value at Series A: 0.50% × $36M = $180,000

- Strike price: Based on 409A valuation, typically ~20% of preferred price.

Phase 4: Series B ($15M at $100M pre-money)

| Stakeholder | Ownership % After Series B |

|---|---|

| Founder A | ~18.5% |

| Founder B | ~18.5% |

| Series A Investors | ~18.5% |

| Series B Investors | ~16.4% |

| ESOP Pool + Employees | ~14.8% |

| Engineer (diluted from 0.50%) | ~0.41% |

Phase 5: Acquisition at $250M

- Engineer's ownership: ~0.41%

- Gross payout: $250M × 0.41% = $1,025,000

- Less strike price cost: 108,250 × $0.10 = $10,825

- Net pre-tax: ~$1,014,175

MODULE 4: EQUITY VEHICLES, VESTING & OPTION MECHANICS

Common Stock vs. Preferred Stock

Common Stock: Held by founders and employees. Lower priority during liquidation. Usually carries voting rights.

Preferred Stock: Held by VCs. Carries special rights negotiated at each round:

- 1x Non-Participating Preferred: Investors get back their investment (1x), then common holders split the remainder. Standard and fair.

- 1x Participating Preferred ("Double Dip"): Investors get their 1x back AND participate in remaining proceeds alongside common holders. This dramatically reduces employee payouts in small exits.

| Structure | Investor Gets (exit at $30M, $10M invested) | Employees Get (15%) |

|---|---|---|

| 1x Non-Participating | $10M back, or convert to equity | ~$3M |

| 1x Participating ("Double Dip") | $10M + 35% of remaining $20M = $17M | ~$1.95M (35% less!) |

Always ask: "Is the preferred stock participating or non-participating?"

The Liquidation Waterfall

In any acquisition, cash flows in strict order:

This is not rare. It's a common outcome in acqui-hire acquisitions.

Option Types: ISOs vs. NSOs

Stock Options

|

+--------> ISOs (Incentive Stock Options)

| - US W2 employees ONLY

| - Favorable capital gains tax treatment in the US

| - $100k annual ISO limit per year

|

+--------> NSOs (Non-Qualified Stock Options) ← International contractors

- Taxed as ordinary income at exercise on the spread

- No annual limitThe NSO Tax Trap: When you exercise NSOs, the "spread" (FMV - Strike Price) is treated as ordinary income immediately — even if the company is private, you cannot sell the shares, and you received no cash. You owe tax on illiquid paper wealth. Covered in Module 5.

Restricted Stock Units (RSUs)

RSUs are a promise to give you actual shares — no strike price required.

- Standard RSUs: Tax triggered at vesting. Common at Series C+ and public companies.

- Double-Trigger RSUs: Shares vest only when BOTH a time milestone AND a liquidity event (IPO, acquisition) occur — protects employees from tax on illiquid shares.

The 4-Year Vesting Schedule with 1-Year Cliff

- Leave at Month 11 Day 29 → 0 options.

- Leave at Month 12 Day 1 → 25% of total grant.

- After the cliff: 1/36th of remaining 75% per month.

Acceleration Clauses

Single-Trigger: All unvested options vest immediately upon acquisition. Favorable to you, but rare for non-executive engineers.

Double-Trigger: Unvested options vest only if BOTH conditions are met:

- Company is acquired

- You are terminated or demoted within 12-24 months of acquisition

Why it matters: In an acqui-hire, the acquirer often fires engineers who don't fit. Without double-trigger protection, you lose unvested equity at the exact moment you lose your job. Negotiate for double-trigger, at minimum.

MODULE 5: INDIAN TAX COMPLIANCE FOR REMOTE EQUITY HOLDERS

This is the most underrated and dangerous module. Many Indian engineers working remotely for US startups unknowingly commit serious tax violations simply because nobody told them these rules.

The Taxation Lifecycle of NSOs

At Grant → No Tax

When the board grants your options, there is zero tax liability.

During Vesting → No Tax

As options vest monthly over 4 years, there is still zero tax. You hold rights, not shares.

At Exercise → PERQUISITE TAX (The Dangerous One)

When you exercise your vested options, the Indian Income Tax Department treats the "spread" as employment income (perquisite).

Taxable Perquisite = (Fair Market Value on Exercise Date − Strike Price) × Number of Shares ExercisedThis entire amount is added to your annual income and taxed at your applicable slab rate.

| Income Slab | Tax Rate (FY 2025-26, New Regime) |

|---|---|

| Up to ₹3 Lakhs | 0% |

| ₹3L to ₹7L | 5% |

| ₹7L to ₹10L | 10% |

| ₹10L to ₹12L | 15% |

| ₹12L to ₹15L | 20% |

| Above ₹15L | 30% |

The Nightmare Scenario: You have 50,000 NSOs. Strike price: $0.10. You exercise when the company's 409A FMV is $5.00/share.

- Taxable perquisite: (5.00 - 0.10) × 50,000 = $245,000 (~₹2.04 Crore)

- Indian tax at 30% slab: ₹61.2 Lakhs

- Company is still private. You cannot sell shares.

- You must pay ₹61.2 Lakhs in CASH out of pocket.

The Strategy: Do NOT exercise early unless a liquidity event is imminent. Keep options as vested-but-unexercised (holding them costs zero cash) until:

- The company announces an acquisition/IPO

- A secondary sale window opens (platforms like Carta, EquityBee, or Forge Global)

- You have certainty the company will succeed and have cash for the tax bill

At Sale → Capital Gains Tax

For Foreign Unlisted Shares (Pre-IPO startup shares):

- Short-Term Capital Gains (STCG): Held ≤ 24 months → Taxed at your slab rate (up to 30% + surcharge)

- Long-Term Capital Gains (LTCG): Held > 24 months → Taxed at 20% with indexation benefit

Capital Gain = (Sale Price − FMV at Exercise Date) × Number of Shares SoldNote: FMV at exercise is the cost basis — the perquisite tax you already paid is NOT double-taxed here.

The DTAA (Double Taxation Avoidance Agreement) Shield

India has a tax treaty with the United States. If your US employer withholds US tax on your income, you can claim credit in India to avoid double taxation.

Your Practical Steps:

- Submit Form W-8BEN to your US startup's HR/Finance team before your first payment. This certifies you are a foreign person and invokes the India-US DTAA, preventing US withholding tax on your salary.

- Declare all US-sourced income in your Indian ITR in the correct schedule.

- If US tax was withheld despite W-8BEN, claim it as Foreign Tax Credit (FTC) in your ITR using Schedule TR (Tax Relief).

🚨 SCHEDULE FA — THE MOST CRITICAL COMPLIANCE REQUIREMENT

This is the regulation most Indian engineers with foreign equity violate unknowingly.

The Rule: Under FEMA and the Black Money Act 2015, any Indian resident holding a foreign financial asset (including unvested or vested stock options in a US company) MUST:

- File ITR-2 or ITR-3 (NOT the simple ITR-1 Sahaj)

- Complete Schedule FA (Foreign Assets) disclosing:

- Name and address of the US startup

- Nature of the asset (Stock Options / ESOP)

- Number of shares / options held

- Value of the asset

- Income derived from it

The Penalty for Non-Disclosure: Under Section 42 of the Black Money Act, the penalty is a flat ₹10 Lakhs per assessment year for failure to disclose foreign assets — even if the asset was legitimately earned, properly taxed, and you had no intent to hide it. The law does not care about intent.

Criminal prosecution under Section 50 can result in imprisonment of 3 to 10 years.

Action Plan:

- From the moment you receive your option grant agreement, engage a CA specializing in international tax and FEMA compliance.

- Budget approximately ₹15,000-₹30,000 per year for proper ITR filing with Schedule FA.

- File every year, even years when you have not exercised any options.

The FEMA General Permission

Good news: You do not need RBI permission to receive stock options as an employee/contractor of a foreign company. Under FEMA Notification No. 4 / 2000-RB, Indian residents are permitted to acquire shares of foreign companies under ESOP schemes offered by their employer without prior RBI approval.

MODULE 6: REAL-WORLD CASE STUDIES

Case Study 1: Supabase (YC W20 — Open-Source Firebase Alternative)

The Journey:

- 2020 Seed: $6M raised at ~$25M valuation. ~10 engineers. Building an open-source PostgreSQL backend platform.

- 2021 Series A: $30M raised at $100M+ valuation. Team grew to ~30 people.

- 2022 Series B: $80M raised at $500M+ valuation. ~80 people globally.

- 2024 Series C: $200M raised. Valuation estimated at $2B+.

Compensation Model (Remote Engineers, 2020-2021):

- Base Cash: $40,000-$65,000 USD/year for remote senior engineers (India/EU/LATAM)

- Equity: 0.30%-0.80% for early senior hires

- Culture: Fully async, remote-first, open-source obsessives

The Equity Math for an Early Engineer (2020, 0.50% grant):

- Paper value at Seed: 0.50% × $25M = $125,000

- After Series A dilution (~20%): 0.40% × $100M = $400,000

- After Series B dilution (~15%): 0.34% × $500M = $1,700,000

- At the $2B+ valuation: 0.29% × $2,000,000,000 = $5,800,000

What engineers can learn: Supabase is open-source and dev-tool focused. Contributing meaningful PRs to their GitHub is the highest-leverage way to get noticed by their hiring team. They hire based on demonstrated OSS ability, not resumes.

Case Study 2: Vercel (Next.js Infrastructure)

The Journey:

- 2020 Series A: $21M at ~$80M valuation

- 2021 Series B: $40M at ~$200M valuation

- 2021 Series C: $102M at $1.1B valuation

- 2022 Series D: $150M at $2.5B valuation

Vercel specifically targeted engineers who had meaningful Next.js and React ecosystem contributions. Many were hired because of their open-source reputation rather than traditional interview paths.

The Equity Math for a Series A Engineer (0.25% grant):

- After 40% total dilution through subsequent rounds: ~0.15%

- At $2.5B valuation: 0.15% × $2,500,000,000 = $3,750,000

- At a potential IPO at $5B valuation: 0.15% × $5,000,000,000 = $7,500,000

Key Insight: Building high-quality open-source tooling and writing about engineering decisions is the single best path into elite infrastructure company hiring pipelines.

Case Study 3: Cal.com (YC W22 — Open-Source Calendly)

The Journey:

- 2022: Raised $32M Series A. Open-source scheduling infrastructure.

- Fully remote, 40+ contributors globally, heavy OSS contributor hiring culture.

Why this is a compelling target for remote engineers:

- TypeScript/Next.js stack — dominant in modern engineering portfolios

- Open-source — PRs and contributions are reviewed publicly

- YC-backed — direct access to the YC hiring network

- Remote-first — explicitly hire globally

The Hiring Pathway:

- Fork Cal.com and run it locally

- Pick a "good first issue" from their GitHub

- Submit a quality PR

- Join their Discord and engage actively

- After 2-3 merged PRs, message the CTO directly on X/Twitter with your contributions

Case Study 4: Dub.co (YC W23 — Open-Source Link Management)

Stack: Next.js 14, TypeScript, Prisma, PlanetScale, Upstash Redis, Tinybird Raise: Seed-stage, YC-backed Culture: Small team (under 10), fully async, open-source first

The entire codebase is Next.js 14 App Router + TypeScript — making contributions accessible to engineers who have built similar stacks. Companies like this are ideal entry points: small enough that your contributions matter, OSS enough that your work is visible, and YC-backed enough that growth trajectories are credible.

MODULE 7: 10 EQUITY TRAPS THAT DESTROY ENGINEER PAYOUTS

Founders are not always evil, but they are optimizing for their company — not for you. Know these traps cold before you sign anything.

🔴 TRAP 1: The "Number of Options" Without Context

The Setup: A founder says: "We're giving you 100,000 options!" You think that sounds massive.

The Reality: The number of options is completely meaningless without knowing the total outstanding shares. 100,000 options in a company with 100,000,000 total shares = 0.10%. The same 100,000 options in a company with 5,000,000 total shares = 2.0% — 20x more valuable.

The Fix: Always ask:

"Could you share the total fully diluted share count so I can calculate my ownership percentage?"

A founder who refuses to share this is a red flag in itself.

🔴 TRAP 2: The High Strike Price Trap

The Setup: A startup raises at a high valuation. Their 409A appraisal sets the common stock FMV high. Your strike price is set at that high FMV.

The Danger: Your strike price might be $2.00/share. For your options to be "in the money," the acquisition price must exceed $2.00/share. If the company sells at $1.50/share, your options are worthless underwater options — you would pay more to exercise than you'd receive.

This happens most often when joining after a Series B or C at a high valuation, especially in the post-2021 AI hype period with inflated multiples.

The Fix: Ask for your strike price explicitly and compare it to the latest preferred price. If the strike price is more than 30% of the preferred price, the discount built into your 409A is thin.

🔴 TRAP 3: The "Phantom Equity" Promise

The Setup: A pre-seed founder says: "We don't have formal equity set up yet, but we'll definitely give you a significant chunk when we incorporate properly."

The Reality: This is a verbal promise with zero legal standing. Without a board-approved Stock Option Agreement, you have nothing. Founders forget, relationships sour, cap tables get complicated. Verbal equity promises are legally unenforceable in almost every jurisdiction.

Documented Cases: There are hundreds of startup lawsuits where early employees worked for below-market salaries under verbal equity promises only to receive nothing when the company was acquired.

The Fix: Refuse to start working at below-market rates without a signed, board-approved equity grant document. If they cannot formalize the equity in 2 weeks, they are not organized enough to be a reliable employer.

🔴 TRAP 4: The Option Expiration Window

The Setup: Your employment ends. Your option grant agreement has a 90-day exercise window after termination. If you don't exercise within 90 days, your vested options expire and you lose them permanently.

The Danger for Indian Remote Contractors: The NSO exercise triggers an immediate Indian tax liability on the spread. You might need to pay ₹20-50 Lakhs in taxes within 90 days of losing your job — in cash, for illiquid shares in a private company.

- Cash-rich scenario: You have savings, exercise, pay the tax, hold shares, hope for an exit.

- Cash-poor scenario: You cannot afford the tax bill, don't exercise, and 90 days later your 3 years of vested equity evaporates to zero.

The Fix:

- Negotiate an Extended Exercise Window (EEW) — ideally 5-10 years post-termination. Companies like Asana, Pinterest, and MongoDB adopted this voluntarily.

- Keep a cash reserve equal to 150% of your estimated exercise tax liability at all times.

🔴 TRAP 5: Participating Preferred with Multiple Liquidation Preferences

The Setup: Investors have 2x or 3x liquidation preferences with full participation rights. Common in down rounds.

The Math:

- Company raises $10M at 2x participating preferred.

- Company is acquired for $40M.

- Investors get: $20M (2x) + 35% of remaining $20M ($7M) = $27M total

- Employees and founders split $13M (instead of the expected ~$26M)

- Your 0.50% grant = 0.50% × $13M = $65,000 instead of 0.50% × $40M = $200,000

The Fix: Ask: "What are the liquidation preference terms on each class of preferred stock?" Run the waterfall math yourself under different exit scenarios.

🔴 TRAP 6: The Down Round Dilution Cascade

The Setup: You join at a $15M valuation with 0.50% equity. The startup misses growth targets. The next round is a down round at $10M. Down rounds trigger anti-dilution protection for investors, causing severe dilution to founders and employees.

Anti-Dilution Mechanisms:

- Full Ratchet Anti-Dilution: Investor's ownership is reset to match the new lower price. Catastrophic dilution to all common stockholders.

- Broad-Based Weighted Average (BBWA): More moderate approach. Standard in YC-style deals.

In a down round with BBWA anti-dilution, employees typically see 25%-50% of their equity value evaporate. Options may also go "underwater."

The Fix: Ask "Has the company raised any flat or down rounds?" and "What anti-dilution provisions are in place?"

🔴 TRAP 7: The Acqui-Hire Retention Package Swap

The Setup: Company is acquired for its engineering team, not its product. The acquirer:

- Pays founders a nominal sum (barely returns their investment)

- Offers engineers attractive new retention packages (cash + RSUs in the acquirer)

- Lets existing startup equity pay out near-zero due to liquidation preferences

The Psychology Trap: The retention package looks generous. You sign it happily, unknowingly giving up vested startup equity with zero additional negotiation.

The Fix:

- Before signing any retention agreement, calculate your startup equity payout in the acquisition waterfall.

- If the payout is tiny ($0-$5,000), the retention package may be a fair replacement.

- If your vested equity should pay out $80,000+, negotiate the retention to be additive (paid on top of equity payout), not in lieu of it.

🔴 TRAP 8: Misclassification as Contractor vs. Employee

The Setup: US startups hiring Indian remote workers almost always classify them as independent contractors. Some contractor agreements explicitly state contractors are not entitled to equity or stock options.

The Equity Danger: You sign the agreement without reading page 47, discover at Month 18 that your verbal equity promise was never in the contractor agreement, and you have no legal claim.

The Indian Tax Danger: As a contractor, you must:

- Register for GST if annual receipts exceed ₹20 Lakhs

- Deduct your own TDS/advance tax — no employer withholding

- File ITR-3 (Business & Profession income) rather than ITR-1

- Maintain proper invoice records in INR and USD

The Fix: Before signing, verify the contractor agreement explicitly mentions your equity grant by name, shares, vesting schedule, and strike price. Set up proper GST registration and quarterly advance tax payments from Day 1.

🔴 TRAP 9: The Post-Money SAFE Stacking Problem

The Setup: A startup raised $4 Million across 10 separate SAFE notes over 2 years against a $12M post-money cap. When these all convert at Series A, the total SAFE dilution to founders and employees is 33% ($4M / $12M) — not the 20% the founders may have casually quoted.

What This Means: The cumulative effect of multiple SAFEs can significantly surprise founders and employees at Series A conversion. Ask: "How much total SAFE capital has been raised, and at what post-money caps?" Compute the total dilution yourself.

🔴 TRAP 10: The Verbal Salary Offer Without Written Confirmation

The Setup: A founder makes a verbal offer of "$24,000/year + 0.50% equity" on a call. You give notice elsewhere. 2 weeks later, the written offer arrives with "$18,000/year + 0.25% equity."

This is not necessarily fraud — founder memories are imperfect and board approvals sometimes come back lower. But the outcome is the same for you.

The Fix: After every verbal offer call, immediately send a confirmation email:

"Thank you for the offer! To confirm what we discussed: base salary of $24,000/year, equity grant of 0.50% (with standard 4-year vesting / 1-year cliff), and a remote contractor structure. Looking forward to the formal offer letter!"

This creates a documented paper trail. If the written offer differs materially, you can reference this email and negotiate from documented truth.

🟡 Things That Look Bad But Aren't

Not Profitable (EBITDA Negative): Completely normal for seed or Series A startups. They are intentionally burning cash to grow. Not profitable ≠ failing. The question is: healthy runway (18+ months) and growing ARR?

No Brand Recognition: YC batches produce hundreds of companies most people have never heard of. Many of the most valuable acquisitions were companies with zero consumer brand awareness. Focus on founding team strength, market size, product-market fit signals, and burn rate.

Small Team Size: A 5-person seed startup is a sign of equity opportunity, not weakness. The earlier you join, the larger your potential grant.

First-Time Founders: YC has an extraordinary track record with first-timers — Airbnb, Stripe, DoorDash, Reddit were all first-time founders. What matters: clarity of vision, product obsession, coachability, and iteration speed.

MODULE 8: EVALUATING YOUR OFFER — A FRAMEWORK

The 3-Tier Compensation Framework

| Tier | Annual Base (USD) | Equity Grant | When to Accept |

|---|---|---|---|

| Floor — Minimum Acceptable | $10,000-$15,000 | 0.75%-1.50% | Only for legendary founders (second-time, successful exits), exceptional product in a massive market, "Founding Engineer" title |

| Target — Primary Goal | $18,000-$30,000 | 0.40%-0.75% | Seed/post-seed YC company, 5-12 people, $2M-$5M raised, $10M-$20M valuation. Strong product, credible founders. |

| Stretch — Optimal Outcome | $36,000-$60,000 | 0.20%-0.40% | Well-funded Seed or Series A, $5M-$15M raised, $25M-$60M valuation, institutional VC backing |

The general principle: the earlier you join and the less cash you take, the more equity you should extract. Founders who aren't willing to trade equity for your below-market salary aren't serious about building long-term alignment.

The 409A Strike Price Calculation

When you receive an offer, ask for the strike price. Then run this math:

Scenario: Offered 75,000 options at $0.08 strike price.

- Cost to exercise all 75,000 options: 75,000 × $0.08 = $6,000 (trivial)

- Company at a $15M valuation → your 0.50% = $75,000 paper value

- At acquisition for $100M → 0.40% (post-dilution) = $400,000

A low strike price means a low exercise cost, which means less tax risk and more profit on exit.

MODULE 9: THE NEGOTIATION PLAYBOOK

Script 1: Confirming a Verbal Offer in Writing

Send within 1 hour of the call.

Subject: Re: Offer Discussion — Confirming Details

"Hey [Founder Name],

Thank you for the offer call today. I'm genuinely excited about what you're building at [Company]. To make sure we're aligned before I review the formal documents, here's my understanding of the package we discussed:

• Base Cash: $[X]/year paid monthly as a contractor • Equity Grant: [X]% ([X,000] options) with standard 4-year vesting and 1-year cliff • Start Date: [Date] • Structure: Independent contractor (with option grant formalized via board-approved agreement)

Looking forward to the formal offer letter! Let me know if anything needs clarification."

Script 2: Unlocking the Share Count Black Box

"Hey [Founder],

I'm very excited about the option package. To help me fully understand the long-term value, could you share a few quick numbers? 1. Total fully diluted share count (including all outstanding options and SAFEs) 2. The post-money valuation from your last round 3. The current 409A strike price for common shares 4. Whether the vesting is monthly after a 1-year cliff

This helps me run the ownership math and confirm my alignment. Really appreciate the transparency!"

Script 3: Trading Cash for Equity

"Hey [Founder Name],

I've thought carefully about the offer and I want to make it easy for us to move forward. I understand cash conservation is critical at the seed stage, and I want to be a long-term stakeholder in [Company]'s success — not just a contractor.

I'm comfortable accepting a lower base of $[X]/year to protect runway. In exchange, I'd like to scale the equity from [current offer]% to [target]%. This aligns my incentives completely with the company's success and makes me an owner from Day 1.

How does that work for you?"

Script 4: Requesting Extended Exercise Window

"One thing I'd like to include in the option agreement is an extended post-termination exercise window — ideally 5 years rather than the standard 90 days. As a remote contractor, the 90-day window creates a difficult tax situation where I'd need to exercise (and pay income tax on the spread) while shares are still illiquid.

Companies like Asana, MongoDB, and Quora have adopted this policy to be engineer-friendly. It costs the company nothing unless there's a liquidity event, and it ensures I can participate fully in the outcome we build together.

Is this something the board would consider?"

Script 5: Handling "Our Bands Are Fixed"

"I completely respect the need to maintain equity hygiene and consistent bands across the team. Since adjusting the base grant isn't possible, could we structure a milestone-based performance grant?

For example: if I successfully ship [Core Feature / Architecture Migration / Integration] within my first 90 days, the board approves an additional 0.15%-0.25% performance grant.

This keeps the initial offer clean and consistent while rewarding demonstrable execution speed. I'm very confident in my ability to earn it quickly."

MODULE 10: PRE-SIGNING DUE DILIGENCE CHECKLIST

Use this before signing any offer letter or option agreement. Do not skip a single item.

Financial Health Checks

- Asked for and received the company's monthly net burn rate

- Calculated runway: Cash on Hand / Net Burn ≥ 18 months

- Verified ARR and MRR are growing (not flat or declining)

- Confirmed the last fundraising round was a flat or up round (not a down round)

- Asked whether any convertible notes have maturity dates within 12 months

Equity Package Checks

- Received the total fully diluted share count in writing

- Calculated exact ownership percentage (Shares Granted / Total Shares)

- Received the 409A valuation report or confirmed current common stock FMV

- Confirmed the strike price is below 30% of the latest preferred price

- Verified the vesting schedule: 4 years, monthly after 1-year cliff

- Confirmed equity grant documented in a board-approved Stock Option Agreement

- Checked whether preferred stock is participating or non-participating

- Asked about liquidation preferences (1x, 2x?) on each class of preferred

- Asked whether there is an extended exercise window (or negotiated 5-year EEW)

- Confirmed acceleration clause: single-trigger or double-trigger on acquisition

Legal & Structural Checks

- Confirmed the company is properly incorporated (Delaware C-Corp for US startups)

- Verified the option grant must be board-approved (not just founder-promised)

- Contractor agreement explicitly names and describes the equity grant

- IP assignment clause reviewed — ensure you retain rights to personal projects built outside company time

- Non-compete clause reviewed — Indian non-competes are generally unenforceable, but check for jurisdiction clauses

Indian Compliance Checks

- Will file ITR-3 with Schedule FA from the year the grant is received

- W-8BEN form prepared to submit to US company's finance team

- CA engaged who specializes in international tax and FEMA

- GST registration assessed (mandatory if invoicing exceeds ₹20L/year)

- Advance tax payment schedule set up (quarterly: June 15, Sept 15, Dec 15, March 15)

Quick Reference: One-Page Glossary

| Term | Definition | Your Action |

|---|---|---|

| SAFE | Agreement for future equity — converts at Series A | Ask for post-money cap and total SAFEs raised |

| ARR | Annual Recurring Revenue | Verify growing 2x+ YoY |

| Net Burn | Monthly cash spend minus revenue | Runway = Cash / Net Burn. Demand 18+ months |

| 409A | Common stock valuation for strike price | Lower = better for you. Ask for the number. |

| Cliff | 1-year with no vesting | Leave before Month 12 = zero equity |

| EEW | Extended Exercise Window | Negotiate 5 years to avoid the tax trap |

| Liquidation Preference | VCs paid first in exits | Ask: 1x non-participating only |

| Participating Preferred | VCs paid twice in exits | Avoid. Kills employee payout in small exits |

| Down Round | Fundraising at lower valuation | Triggers anti-dilution, underwater options |

| Acqui-hire | Acquired for team, not product | Negotiate retention additively, not as replacement |

| Schedule FA | Indian tax disclosure of foreign assets | File every year or face ₹10L penalty |

| Double-Trigger | Unvested options accelerate only if fired post-acquisition | Always negotiate for this |

| NSO | Your option type as an international contractor | Taxed as income at exercise, not at grant |

The single most expensive mistake startup engineers make is not the equity they negotiate poorly — it's the equity they lose to traps, expiring windows, underwater strikes, and tax bills they weren't prepared for. Use this as a reference before every offer you receive.